The evolution of the price per barrel of crude oil

5 min read

prices have undergone considerable changes over the decades, particularly during periods of global crisis or as a result of economic developments. Their level is a determining factor in the global economy, given the decisive role of oil in the global .

© PASCAL LAURENT / TotalEnergies - Oil storage tanks in Ho Chi Minh City, Vietnam

The barrel of oil: a key factor in the global economy

For decades, the price of a of crude oil has been as much a geopolitical factor as an economic one. It is based on a traditional unit of measurement dating back to the 19th century, the barrel (equivalent to 159 liters), even though oil is now transported in bulk by pipelines, tankers, and trains.

In fact, it is more accurate to talk about crude oil prices in the plural. This is because the prices set on international markets, mainly New York and London, use different “benchmark crudes,” primarily (North Sea crude) for Europe and WTI (West Texas Intermediate) for North America, which differ from one another and respond to their own laws of supply and demand. There may therefore be different price movements between these crudes.

The first oil shocks: crises and major upheavals

From 1860 to 1940, barrel prices fluctuated according to world events, rising during World War I and falling during the 1929 crisis. Between 1948 and 1970, they remained relatively stable and low, before entering a series of crises known as “oil shocks.”

The “first oil shock” began in 1971 when the Bretton Woods international financial system was abandoned. It intensified in 1973 during the Yom Kippur War, when oil-producing countries in the Arab world announced an embargo against countries supporting Israel. Within a year, the price per barrel had quadrupled.

The Iranian Revolution in 1978 and the Iran-Iraq War in 1980 caused the “second oil shock,” with prices doubling.

2008: the era of extreme fluctuations

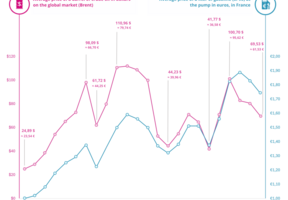

The “third oil shock” refers to an upward trend that began in 2003, driven by growing demand from emerging economies (China, India, Brazil, etc.) and accelerated sharply in the first half of 2008 at the onset of the global economic crisis. The price of Brent crude rose from $96 on January 2, 2008, to $144 on July 3, 2008. The impact on prices was less severe.

The price then plummeted at the height of the financial crisis. The average monthly price of crude oil fell from $130 to $40 per barrel between July and December 2008. From 2009 onwards, as producing countries reduced their output to maintain their income levels, the price per barrel gradually rose to $80.

In 2010, the economic recovery was accompanied by the strongest growth in oil demand since 2004. This contributed to a further rise in prices. This tension intensified in early 2011 with the revolutions in the Arab world, as markets feared repercussions in terms of production capacity.

2014-2016: the collapse of prices and the battle for market share

In the summer of 2014, prices collapsed, falling below the $50 mark at the start of 2015. The main cause was oversupply, fueled by shale oil production in the United States, even though global consumption continued to grow. Determined to defend its market share, Saudi Arabia decided to maintain OPEC production levels. Its aim was to force US producers to reduce their own production. A “standoff” ensued. The price of Brent crude fell below $30 per barrel in January 2016, its lowest level since 2003. The situation became very difficult for some producing countries, such as Venezuela, Algeria, and Russia.

From February 2016, prices rose again, reaching $50 in June 2016, thanks in particular to a decision by Saudi Arabia, Venezuela, Qatar, and Russia to freeze production.

2020 : la pandémie de Covid-19 et ses conséquences inédites

The Covid-19 pandemic caused further severe turbulence, leading to a sharp decline in global economic growth and an almost total halt in tourism from March 2020 onwards. At the height of the crisis in late April, the price of Brent crude fell from $50 to less than $20, a level not seen in 20 years. By June 2020, it had rebounded to $40-45, then to $70 in the summer of 2021.

2022: The war in Ukraine and the new global energy landscape

The price began to soar in January 2022 amid tensions between Russia and Ukraine, which led to the invasion on February 24. It remained above $100 throughout the first half of the year, peaking at $120 in mid-June. It then fluctuated between $70 and $90 as global markets reorganized following Western sanctions on Russian oil. From the summer of 2025, as a new energy map of the world took shape, it fell back to around $65.

Source :

- Suivre les cours (In French)

This may interest you

This may interest you

See all